Rethinking Passenger Mix Risk in Global Airport Retail Strategy

Global airport retail — especially duty free and luxury — did more than grow in the decade leading up to 2019. It consolidated the belief that traffic volume equals revenue growth. But beneath that assumption was a structural reality that the pandemic brutally exposed: growth was not evenly distributed across passengers. It was concentrated.

Table of Contents

- 1. A Quantified Reality Check: Regional and Nationality Spend in Global Airport Retail

- 2. Nationality Spend Intensity: A Modern Lens on Global Airport Retail Revenue

- Behavioural Signals That Drive Global Airport Retail Conversion

- 3. The Revenue Exposure Equation: Quantifying Structural Dependence in Global Airport Retail

- Concentrated Portfolio: What the Numbers Show for Global Airport Retail

- Scenario Stress Test: The EBITDA Risk in Global Airport Retail

- Diversification Works: A Stronger Global Airport Retail Portfolio

- 4. Beyond Nationality: Demographic Shifts Add a Second Layer of Global Airport Retail Risk

- How Millennials and Gen Z Are Reshaping Global Airport Retail Spend

- 5. Four Strategic Imperatives for Global Airport Retail Diversification

- Imperative 1: Dynamic Route Portfolio Design for Global Airport Retail

- Imperative 2: Product Category Alignment

- Imperative 3: Data Driven Segmentation

- Imperative 4: Partnerships and Loyalty Synergies

- 6. Frequently Asked Questions About Global Airport Retail Passenger Mix Risk

- What is passenger mix risk in global airport retail?

- Which nationalities drive the most spend in global airport retail?

- How do you calculate revenue exposure in global airport retail?

- What is the Asia Pacific share of global airport retail?

- Why is diversification a boardroom imperative for global airport retail?

- How are Millennial and Gen Z travellers changing global airport retail?

- What does a diversified global airport retail revenue portfolio look like?

- What are the four strategic imperatives for global airport retail diversification?

- 7. Conclusion: The Future of Global Airport Retail Is Diversified Demand

- Key References

A handful of nationalities and regions disproportionately influenced global airport retail sales. When those corridors paused, the pain was severe precisely because exposure was concentrated. Today the travel ecosystem has reset structurally. The recovery of passenger volumes has been strong but the composition of demand has shifted decisively. For commercial leaders this is not an operational footnote. It is a strategic imperative.

1. A Quantified Reality Check: Regional and Nationality Spend in Global Airport Retail

To understand risk in global airport retail we first need to see the magnitude of dependency that existed before 2020. The table below maps estimated regional shares of global duty free and travel retail sales.

| Region | Estimated Share of Global Airport Retail Sales | Strategic Note |

|---|---|---|

| Asia Pacific | ~40 to 45% of global sales | Highest globally; China dominant within region |

| Europe | ~28 to 30% | Mature market; resilient but lower growth trajectory |

| North America | ~24 to 28% | Strong domestic travel base; growing inbound |

| Middle East and Africa | ~10 to 15% | Fastest growing; UAE hubs gaining significant share |

| Latin America | ~4% | Emerging; underpenetrated relative to passenger growth |

These figures illustrate that global airport retail revenue was heavily anchored in a few regional hubs — with Asia Pacific alone contributing nearly half of the global total. Europe contributed nearly 30% of global duty free revenues. The implication was stark: when one region contributes nearly half of global retail revenue, the revenue model is inherently concentrated.

The Pre-2020 Dependency Reality in Global Airport Retail

Asia Pacific accounted for approximately 45% of global duty free revenues before 2020. Europe contributed nearly 30% of global duty free revenues. Chinese travellers dominated spend intensity globally, followed by UAE and Indian travellers. When one region or nationality contributes nearly half of global retail revenue, the revenue model is inherently concentrated.

Today these shares have rebounded but flows and spend patterns have shifted — with Middle East hubs increasingly benefiting from diversified flows and high spend outbound segments. The structural lesson for global airport retail boards is that recovery does not eliminate concentration risk. It only resets the baseline.

Related: Airport Retail Data and AI Personalisation: Who Owns the Passenger Relationship?

2. Nationality Spend Intensity: A Modern Lens on Global Airport Retail Revenue

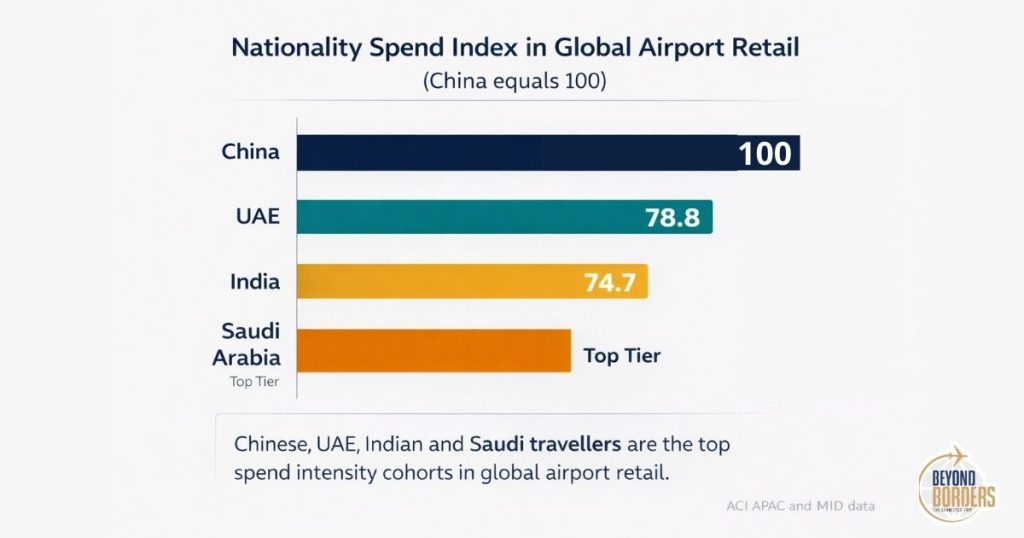

While exact global nationality revenue splits are not universally published by corridor, data from Airports Council International Asia Pacific and Middle East provides relative spend intensity indices that show magnitude and priority for global airport retail operators.

| Nationality | Retail Spend Index (China = 100) | Duty Free Spend Profile in Global Airport Retail |

|---|---|---|

| China | 100 | Highest contributor globally; dominant in duty free and luxury |

| UAE | 78.8 | Second only to China; strong in luxury gifting and fragrances |

| India | 74.7 | High and rapidly growing; emerging as a top tier cohort |

| Saudi Arabia | Top tier | Strong in luxury and gifting segments; GCC influence expanding |

Behavioural Signals That Drive Global Airport Retail Conversion

These indices estimate relative spend contribution rather than absolute revenue but they confirm that Chinese, UAE, Indian and Saudi travellers are the top spend intensity cohorts in global airport retail. The behavioural data reinforces this: a significant portion of Chinese travellers — 58% — plan to shop at airports before departure, highlighting strong intention and conversion potential. These patterns confirm that passenger mix and nationality are leading indicators of spend outcomes, not lagging ones.

The strategic implication for global airport retail leadership is clear: knowing which nationalities are on your routes — and how their spend profiles are evolving — is as commercially critical as knowing your passenger volumes.

3. The Revenue Exposure Equation: Quantifying Structural Dependence in Global Airport Retail

To manage passenger mix risk in global airport retail, boards must measure not just volume but revenue exposure. The formula is straightforward.

Revenue Exposure Formula for Global Airport Retail Boards

Revenue Exposure % = (% of total retail revenue from one nationality) multiplied by (volatility index for that market)

A low volatility index (0.2) reflects a stable outbound travel market with predictable spend patterns.

A high volatility index (0.7) reflects a market with significant geopolitical, economic or travel policy sensitivity.

The higher the combined score, the greater the structural risk to global airport retail commercial performance.

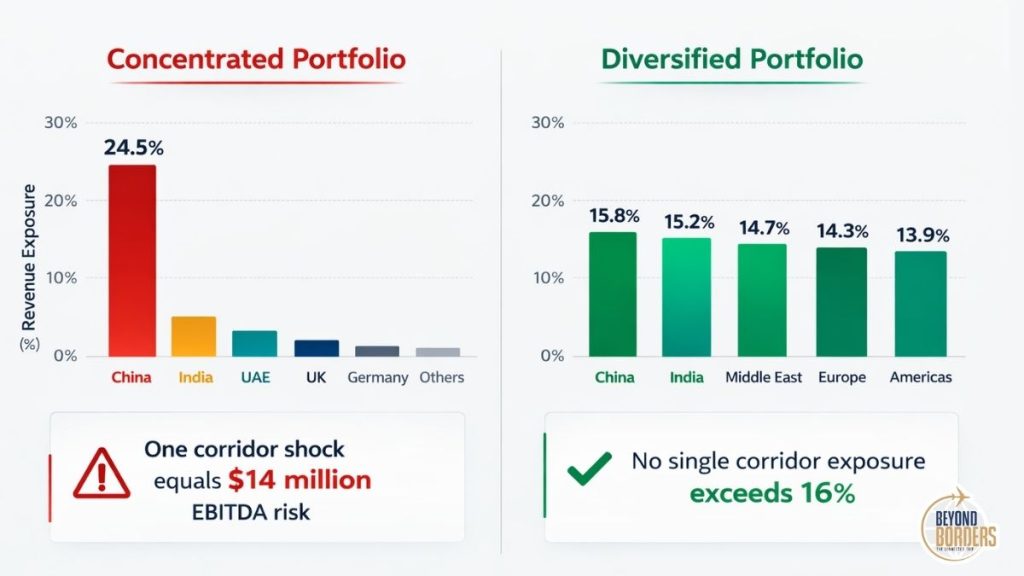

Concentrated Portfolio: What the Numbers Show for Global Airport Retail

The table below applies the revenue exposure model to a hypothetical but realistic global airport retail portfolio concentrated around a few dominant nationalities.

| Nationality | % of Total Retail Revenue | Volatility Index | Revenue Exposure % (Concentrated Portfolio) |

|---|---|---|---|

| China | 35% | 0.7 | 24.5% |

| India | 18% | 0.4 | 7.2% |

| UAE | 14% | 0.3 | 4.2% |

| UK | 10% | 0.2 | 2.0% |

| Germany | 8% | 0.2 | 1.6% |

| Others | 15% | 0.3 | 4.5% |

This model clearly shows that China’s spend intensity and exposure is structurally significant — contributing nearly a quarter of total risk when volatility is factored. For a global airport retail operator generating USD 500 million in annual retail revenue this translates directly into a scenario stress test.

Scenario Stress Test: The EBITDA Risk in Global Airport Retail

Using the concentrated portfolio model: China contributes USD 175 million of USD 500 million in total retail revenue. A 20% decline in Chinese spend equals minus USD 35 million. At a 40% retail margin this equates to minus USD 14 million in EBITDA risk. This is real material risk, not theory.

Diversification Works: A Stronger Global Airport Retail Portfolio

The table below shows the same model applied to a diversified demand portfolio. The contrast is stark.

| Nationality | % of Total Revenue | Volatility Index | Revenue Exposure % (Diversified Portfolio) |

|---|---|---|---|

| China | 22% | 0.7 | 15.4% |

| India | 20% | 0.4 | 8.0% |

| Middle East | 18% | 0.3 | 5.4% |

| Europe | 20% | 0.2 | 4.0% |

| Americas | 20% | 0.3 | 6.0% |

Result: no segment exceeds approximately 16% exposure and volatility is distributed across markets with different sensitivity profiles. This is structural resilience for global airport retail — not a theoretical ideal but a quantifiable strategic outcome.

Related: Travel Retail Strategy: The Five Forces Shaping the Next Decade

4. Beyond Nationality: Demographic Shifts Add a Second Layer of Global Airport Retail Risk

Passenger mix risk in global airport retail is now multi-dimensional. Nationality is one axis but generational cohorts add a second layer of structural change that commercial leaders cannot afford to ignore.

How Millennials and Gen Z Are Reshaping Global Airport Retail Spend

Younger cohorts — Millennial and Gen Z — are not only spending more but spending differently. They allocate higher spend to premium goods, they research online before purchasing in store and they use digital touchpoints throughout the journey. Airports Council International’s latest Retail Study shows that 56% of airports now report commercial revenues exceeding pre-2020 levels despite uneven traffic recovery. Passenger spend intensity is rising with a shift towards behaviour and mix rather than sheer passenger count.

For global airport retail operators this creates a second dimension of risk: assortments and experiences designed for the spending patterns of older high-value cohorts may underperform with younger high- spend travellers. The operator that understands and serves both dimensions simultaneously will build a more resilient commercial portfolio.

5. Four Strategic Imperatives for Global Airport Retail Diversification

To manage nationality and demographic mix risk, global airport retail strategy must evolve from volume optimisation to portfolio management. Four imperatives define this shift.

Imperative 1: Dynamic Route Portfolio Design for Global Airport Retail

Target emerging high spend markets such as India, GCC nations and ASEAN corridors actively. Route development and airline partnership decisions must be evaluated not just for passenger volume but for spend intensity and volatility profile. A new route that brings 500,000 passengers with a 0.3 volatility index and a 74.7 spend intensity is more valuable to global airport retail than one bringing 600,000 passengers with a 0.7 volatility index.

Imperative 2: Product Category Alignment

Match assortments to the spend profiles of top cohorts. Chinese travellers over-index in luxury and premium spirits. UAE and Saudi travellers index highly in fragrances, gifting and premium confectionery. Indian travellers are rapidly growing in premiumisation across multiple categories. Global airport retail operators that build category architecture around actual passenger nationality mix — rather than generic luxury assortments — will convert at higher rates.

Imperative 3: Data Driven Segmentation

Use analytics and CRM to identify high-value profiles early in the journey. Airlines hold nationality and loyalty data. Airports hold dwell time and location data. Where these datasets are connected with passenger consent the commercial opportunity is transformative. A global airport retail operator that can identify a Chinese premium traveller at check in and serve them a targeted offer within 20 minutes of arriving in the duty free zone is operating at the frontier of commercial performance.

Imperative 4: Partnerships and Loyalty Synergies

Align airports, airlines and duty free retailers on shared passenger insights. The structural opportunity in global airport retail is not any single operator’s to own alone. The operators who build genuine data partnerships across the ecosystem — sharing nationality mix intelligence, spend behaviour signals and loyalty programme data — will build the deepest commercial moats.

Related: Data Strategy and Personalisation in the Modern Travel Retail Channel

6. Frequently Asked Questions About Global Airport Retail Passenger Mix Risk

What is passenger mix risk in global airport retail?

Passenger mix risk in global airport retail is the commercial vulnerability that arises when a disproportionate share of total retail revenue is generated by passengers from a single nationality, region or demographic cohort. When that corridor is disrupted by geopolitical events, travel restrictions or economic shocks the impact on retail revenue is amplified by the degree of concentration. The pandemic demonstrated this risk at scale when Asia Pacific flows paused and airports that were heavily dependent on Chinese traveller spend experienced severe revenue compression.

Which nationalities drive the most spend in global airport retail?

Based on ACI Asia Pacific and Middle East spend intensity indices, Chinese travellers hold an index of 100 and are the highest contributor globally. UAE nationals follow at 78.8 and Indian travellers at 74.7, with Saudi Arabian travellers also ranked as a top tier cohort. These four nationalities represent the most commercially significant segments in global airport retail for luxury, premium spirits, fragrances and gifting categories.

How do you calculate revenue exposure in global airport retail?

The revenue exposure formula for global airport retail is: Revenue Exposure percentage equals the percentage of total retail revenue attributable to one nationality multiplied by the volatility index for that market. A low volatility index of 0.2 reflects a stable outbound market. A high index of 0.7 reflects a market with significant geopolitical or policy sensitivity. For example a nationality contributing 35% of revenue with a volatility index of 0.7 generates a revenue exposure of 24.5% — which in a USD 500 million retail portfolio represents over USD 120 million in at-risk revenue.

What is the Asia Pacific share of global airport retail?

Asia Pacific accounts for an estimated 40 to 45% of global duty free and travel retail sales, making it the dominant region by a significant margin. Europe contributes approximately 28 to 30%, North America 24 to 28%, the Middle East and Africa 10 to 15% and Latin America approximately 4%. This concentration means that disruption to Asia Pacific passenger flows — as seen during COVID-19 and during the slow return of Chinese outbound travel — has an outsized impact on the global airport retail industry.

Why is diversification a boardroom imperative for global airport retail?

The post-2020 reset demonstrated that traffic volume alone does not predict revenue resilience in global airport retail. The quality and composition of passenger demand — nationality, spend intensity and volatility profile — is the primary driver of commercial outcomes. Boards that understand and actively manage passenger mix risk through diversified nationality exposure, multi- corridor route strategies and category alignment to top spend cohorts can protect margins and expand them sustainably even through market disruptions.

How are Millennial and Gen Z travellers changing global airport retail?

Airports Council International’s Retail Study shows that younger cohorts are both spending more and spending differently in global airport retail. Millennial’s and Gen Z allocate higher spend to premium goods and use digital touch points extensively for pre-purchase research. This creates a second layer of risk beyond nationality: assortments designed for older high-value cohorts may under perform with younger high-spend travellers. Operators that invest in omnichannel experiences and digital discovery journeys are better positioned to capture this emerging segment.

What does a diversified global airport retail revenue portfolio look like?

A well diversified global airport retail revenue portfolio distributes spend contributions across multiple nationalities and regions such that no single cohort contributes more than approximately 20 to 22% of total revenue. Applying the revenue exposure model, a diversified portfolio might include China at 22%, India at 20%, Middle East at 18%, Europe at 20% and the Americas at 20%. With appropriate volatility indices applied, no single corridor exceeds 15 to 16% exposure — providing structural resilience against individual market disruptions.

What are the four strategic imperatives for global airport retail diversification?

The four imperatives are: first, dynamic route portfolio design that targets emerging high spend markets such as India, GCC nations and ASEAN corridors with route decisions evaluated on spend intensity rather than volume alone; second, product category alignment that matches assortments to the spend profiles of top nationality cohorts; third, data driven segmentation using CRM and analytics to identify high-value passengers early in the journey; fourth, partnerships and loyalty synergies that align airports, airlines and duty free retailers on shared passenger insights to build collective commercial intelligence.

7. Conclusion: The Future of Global Airport Retail Is Diversified Demand

Global airport retail strategy can no longer afford to be volume centric. The past decade was shaped by the dominance of a few spend corridors. The next decade will be shaped by demand quality, diversified exposure and systematic risk management.

Boards that understand, quantify and act on passenger mix risk — with real spend data, nationality indices and scenario models — will not only protect margins but will expand them sustainably. The tools to do this exist. The data is available. What has often been missing is the strategic framework to apply it consistently at the boardroom level.

In global airport retail the future belongs to those who see passenger mix not as an operational metric but as a portfolio management discipline — one that is as central to commercial strategy as route development, concession design and brand curation.

Key References

- ETRC: EU Economic Impact of Duty Free and Travel Retail Report 2025

- ACI Asia Pacific and Middle East: Airport Travel Retail Retail Study

- Gulf News: UAE Travellers Spend Second Only to China, ACI Study

Disclaimer: The analysis, opinions and projections expressed in this article are based on publicly available information and research. They are not intended as professional, legal or policy advice.